Buying a House France: Your Complete Guide

So, you're dreaming of buying a home in France. It’s an exciting thought—a rustic stone farmhouse in the Dordogne, a chic apartment in Paris, or a sun-drenched villa in Provence. The good news is, this dream is more achievable than you might think. It just takes a solid understanding of the market, the legal steps, and the key people who will help you along the way.

The French property market is incredibly diverse. You’ll find half-timbered houses in Normandy, sturdy granite homes in Brittany, and the traditional stone mas (farmhouses) that are so iconic. Getting a feel for these regional differences is part of the fun; you can get a better sense of what’s out there by exploring something specific like real estate in Provence.

This guide will give you a practical roadmap, taking you from the first thoughts about financing all the way to signing the final Acte de Vente.

Understanding the Current Market Climate

The French property market has seen some big changes lately. Transaction volumes have cooled off quite a bit, with existing home sales dropping to levels we haven't seen since 2015.

To put a number on it, the rolling 12-month total for existing home sales hit just 778,000 units last November. That's a year-on-year drop of 11.99%, which is pretty significant. You can dig deeper into these trends and what they mean for buyers in this detailed market analysis from Global Property Guide.

What does this mean for you? This shift is creating a more balanced market, which could give you more negotiating power than buyers have had in years. It’s a good time to be well-informed and ready to move when you find the right place.

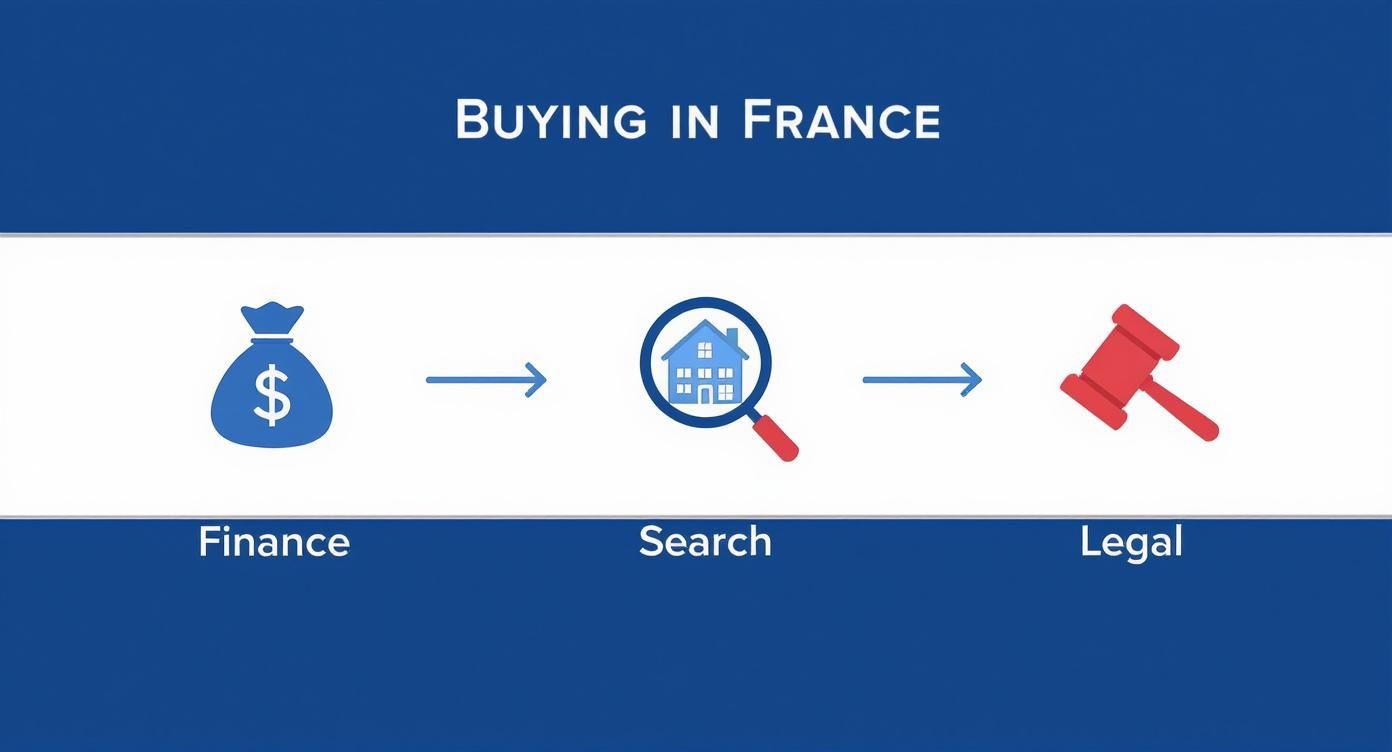

The infographic below gives a great visual overview of the essential stages you’ll go through when buying a house in France.

As you can see, the whole process really boils down to three pillars: getting your finances in order, finding the right property, and navigating the legal paperwork. Master these, and you're well on your way.

The French Property-Buying Process at a Glance

To give you a clearer picture, I've broken down the journey into its core components. While every purchase is unique, nearly all will follow this general timeline.

Key Stages of Buying Property in France

| Stage | Key Objective | Typical Duration |

|---|---|---|

| Initial Research & Budgeting | Determine your budget, get a mortgage pre-approval, and define your search criteria. | 1-3 months |

| Property Search & Viewings | Find suitable properties online or with an agent and conduct in-person visits. | 1-6 months |

| Making an Offer (Offre d'Achat) | Submit a formal written offer to the seller. | 1-2 weeks |

| Signing the Compromis de Vente | Sign the initial sales agreement with the notaire and pay the deposit (usually 5-10%). | 2-4 weeks |

| The 10-Day Cooling-Off Period | A legal period for the buyer to withdraw from the sale without penalty. | 10 days |

| Finalizing the Mortgage | Secure your final mortgage offer from the bank. | 4-8 weeks |

| Signing the Acte de Vente | Sign the final deed of sale, pay the remaining balance, and become the legal owner. | 1 day |

This table lays out the main milestones, but remember that the timeline can stretch or shrink depending on your situation, especially when it comes to financing and any negotiations. The key is to be prepared for each step before it arrives.

Sorting Out Your Finances and Getting a French Mortgage

For most people dreaming of a French property, the financial side of things can feel like the biggest hurdle. It’s true that France has its own way of doing things, but once you understand the landscape, it’s far less intimidating. Getting your finances in order right at the start isn't just a good idea—it's absolutely essential for a smooth ride.

French lenders are notoriously careful. They’re going to want to see a very clear and stable financial picture before they even think about lending, especially to a non-resident. This means getting all your paperwork ready long before you even start looking at properties is non-negotiable.

The All-Important Personal Deposit

In France, your down payment is called the 'apport personnel'. Think of this as more than just a deposit; it's your way of showing the bank you're financially stable and serious about the purchase. While a French resident might get away with a 10% deposit, international buyers need to be ready for higher stakes.

Most French banks will expect a deposit of at least 20-30% of the sale price from a non-resident. If you're a non-EU citizen, don't be surprised if that number creeps up to 40%. This larger sum doesn't just chip away at the property value; it gives the bank confidence that you can handle all the associated costs, like the notary fees.

Getting to Grips with the French Debt-to-Income Ratio

French banks live by a strict rule called the 'taux d'endettement', or debt-to-income ratio. This isn't a guideline—it's a hard and fast calculation that can make or break your mortgage application.

The High Council for Financial Stability (HCSF) in France has capped this ratio at 35%. What this means is that your total monthly debt payments cannot be more than 35% of your gross monthly income. This includes everything: the new French mortgage, any mortgages back home, car payments, and any other loans you might have.

Let's break that down. Say your gross household income is €6,000 per month. Your total monthly debt payments can't go over €2,100 (€6,000 x 0.35). If you already have €600 in existing monthly loan payments, a French lender will only approve a mortgage with monthly repayments of up to €1,500.

This rigid formula is exactly why getting a mortgage pre-approval is so critical. It gives you a realistic borrowing figure before you fall in love with a property you can't afford.

Assembling Your Document Dossier

When you're ready to apply for a French mortgage, you'll need to submit a comprehensive file of your financial life. Lenders are meticulous, so being organized is your best friend. You're essentially creating a financial CV to prove you're a reliable borrower.

Be prepared to provide the following:

- Proof of Identity: Passports and birth certificates for everyone on the application.

- Proof of Address: Recent utility bills or bank statements from the last three months.

- Income Verification: Your last three months of payslips, your most recent P60 (if you're in the UK), and your last two years of tax returns.

- Bank Statements: The last three to six months of statements from all of your main accounts, showing your salary coming in and your regular outgoings.

- Proof of Deposit: A clear statement showing you hold the funds for your 'apport personnel'.

If you're self-employed, the list gets longer. You'll typically need to show at least three years of certified company accounts and personal tax returns to prove your earnings are stable and consistent.

French Banks vs. International Lenders

When you're looking for financing, you've got a few options. You can go directly to a French bank, work with a specialist mortgage broker, or even try to get a loan from a lender in your home country. Each route has its upsides and downsides.

For a much deeper look into this, check out our guide on how to get a mortgage for a foreign property, which really gets into the nitty-gritty of international lending.

Comparing your options is a key part of the process. Here’s a quick overview to help you figure out what might work best for you.

Lender Comparison

| Lender Type | Pros | Cons |

|---|---|---|

| French Banks | Generally offer better interest rates and loan conditions. | Can be bureaucratic, demand extensive translated documents, and may be wary of non-residents. |

| International Lenders | Often have a better grasp of your home country's financial setup and offer services in English. | Rates might be higher, and they may not be as familiar with the specifics of the French legal process. |

| Mortgage Brokers | Offer expert advice, have access to many lenders, and can bridge any language gaps. | Their services come with a fee, but it's often money well spent for the time and stress you'll save. |

In my experience, the most effective route is often working with a specialist mortgage broker who truly understands the French market for international buyers. They know how to present your application in the best possible way and can navigate the unique demands of different French banks for you, which can massively boost your chances of getting that "yes."

Finding Your Property and Making an Offer

Once you have your mortgage pre-approval sorted, you get to start the fun part: the actual hunt for your French home. This is where those daydreams of rustic farmhouses or chic city apartments start feeling real. To do it right, you need to know where to look and, just as importantly, how to act when you find "the one."

Where to Start Your Search

The search itself can be a wonderful journey through France's incredibly diverse regions. Online property portals are the obvious first stop.

Websites like SeLoger and LeBonCoin are the heavy hitters in France. They have a massive selection of listings from both agents and private sellers, so you get a great feel for what's out there.

If you're buying from abroad, you'll also find sites like Green-Acres or French-Property.com really helpful. They're built for international buyers, often with listings and information in English.

Getting an Agent on Your Side

Browsing online is one thing, but nothing replaces the local knowledge of a good 'agent immobilier' (real estate agent). They bring so much to the table—insider info on the best neighborhoods, alerts about properties before they even hit the market, and a steady hand to guide you through negotiations and paperwork.

Finding the right agent is a game-changer. Our guide on how to choose a real estate agent is packed with practical tips to help you find a pro who really gets what you're looking for. Their local insight isn't just a nice-to-have; it can save you a ton of time, stress, and money.

When you start viewing properties, try to look past the beautiful staging. Your focus should be on the bones of the house.

- The Big Stuff: Keep a sharp eye out for signs of damp, any cracks in the walls, or a roof that looks past its prime. These are the fixes that can really drain your bank account.

- The Systems: Ask about the age and condition of the plumbing, the electrical system (électricité), and the heating (chauffage).

- The Diagnostics: The seller is required by law to give you a file of technical reports called the 'Dossier de Diagnostic Technique' (DDT). This is a goldmine of information, with reports on energy performance (DPE), asbestos, lead, termites, and more. Read it carefully.

Making Your Move

As you search, it’s smart to get a feel for the market. French house prices have been doing some interesting things lately. The national House Price Index (HPI) was 126.30 points in Q2 of last year, down a touch from 126.54 points the previous quarter. The year-on-year increase was only 0.50%, which tells us prices have mostly flattened out. You can dig into these French housing index trends on Trading Economics for more detail.

This market stabilization is actually good news for buyers. It often means there’s more room to negotiate than when prices are shooting up.

Found a place you love? It’s time to make an offer. Forget what you might be used to—in France, a verbal offer means nothing. You have to submit a formal written offer, or 'offre d'achat'. This isn't just a casual note; if the seller accepts it, it becomes a real commitment to buy.

Your written offer needs to be airtight. It must state the price you're offering, include a clear description of the property, and set a time limit for the seller to respond (usually a week or two). But the most important part? Adding your protective conditions.

How to Craft a Smart, Protected Offer

The real power of your 'offre d'achat' lies in the 'clauses suspensives'—your conditional clauses. Think of these as your escape hatches. They let you walk away from the deal without losing your deposit if certain critical conditions aren't met.

Here are the absolute must-haves:

- Subject to Financing ('clause de condition d'obtention de prêt'): This is non-negotiable. It states that the sale only goes through if you successfully secure your mortgage.

- Subject to Satisfactory Surveys: Especially for older homes, you can make the offer conditional on getting clean structural surveys that don't reveal any nasty surprises.

- Subject to Planning Permission: If your dream involves adding a pool or building an extension, this clause makes the sale dependent on you getting the green light (permis de construire) from the local authorities.

Including these conditions turns your offer from a simple bid into a secure, well-thought-out plan. It protects you and ensures you aren't locked into a purchase that no longer works for you.

Navigating the French Legal Process

Once your offer is accepted, you step into the legal side of buying a house in France. Be prepared, because it’s a world away from the process you might know back home. It's structured, heavily regulated, and designed to protect everyone involved.

The central figure orchestrating everything is the notaire, a highly qualified lawyer and public official appointed by the Ministry of Justice. Think of them not as your personal lawyer, but as a neutral arbiter for the state. Their job is to make sure the sale is legally sound, all taxes are paid, and the property title is transferred without a hitch.

While the seller often has their own notaire, you have every right to appoint your own. The best part? It doesn’t cost you extra. The fee is simply split between the two offices, and it gives you peace of mind having your own representative in the mix.

The Compromis de Vente: The First Big Step

The first major legal document you’ll encounter is the 'Compromis de Vente'. Don’t mistake this for a simple agreement—it’s a legally binding preliminary sales contract that locks in both you and the seller. Once you've both signed, the seller can't entertain a higher offer or change their mind.

This contract lays out all the critical details: the price, a full description of the property, and the all-important 'clauses suspensives' (conditional clauses). These are your safety nets, like making the sale dependent on securing a mortgage. You'll pay a deposit, usually between 5-10% of the purchase price, which is held safely in the notaire's escrow account.

The importance of this stage is clear in the current market. As things pick up, the number of 'compromis de vente' being signed has jumped by 20% year-on-year. This shows a real rush of committed buyers, so being ready for this binding step is essential. You can find more great insights on the French property market recovery on My-French-House.com.

Your 10-Day Cooling-Off Period

French law gives buyers a fantastic protection called the 'délai de rétractation'—a 10-day cooling-off period.

This period starts the day after you receive your copy of the fully signed 'Compromis de Vente'. For ten days, you can walk away from the purchase for any reason at all, no questions asked and no penalties. If you do decide to pull out, you must send a formal letter by registered post ('lettre recommandée avec avis de réception') to the notaire. Miss that deadline, and your deposit is on the line.

Understanding the Mandatory Property Surveys

Tucked into the 'Compromis de Vente' is a thick file of reports called the 'Dossier de Diagnostic Technique' (DDT). The seller is legally required to provide these, and they give you a fairly comprehensive overview of the property's health.

The DDT bundle typically includes surveys on:

- Energy Performance (DPE): Grades the home’s energy efficiency from A to G. This is crucial for investors, as properties rated F or G now face rental restrictions.

- Asbestos ('Amiante'): Mandatory for any property built before July 1997.

- Lead ('Plomb'): Required for homes built before 1949.

- Termites ('Termites'): A must-have in designated high-risk areas.

- Natural and Industrial Risks (ERNMT): Outlines potential local risks like flooding or industrial pollution.

- Gas and Electrical Installations: A safety check on any systems that are over 15 years old.

These reports aren't a guarantee of a perfect home, but they’re invaluable for flagging potential problems and future expenses you’ll need to budget for.

The Final Acte de Vente

After the 'Compromis' is signed and all your conditions are met—a process that usually takes two to three months—it’s time for the grand finale: signing the 'Acte de Vente'. This is the final deed of sale, and it’s a formal affair that takes place at the notaire’s office.

This is the moment it all becomes real. The notaire reads the entire deed aloud to ensure complete transparency. You’ll pay the remaining balance of the purchase price, plus the notaire’s fees and taxes. Once the ink is dry, the keys to your new French home are officially yours.

To really nail down the difference between these two critical contracts, here’s a quick breakdown.

Compromis de Vente vs Acte de Vente

| Feature | Compromis de Vente (Preliminary Agreement) | Acte de Vente (Final Deed) |

|---|---|---|

| Purpose | To legally bind the buyer and seller to the sale under specific conditions. | To officially transfer legal ownership of the property to the buyer. |

| Timing | Signed 2-4 weeks after the offer is accepted. | Signed 2-3 months after the Compromis de Vente. |

| Legal Weight | A binding contract, but conditional. | The final, unconditional transfer of title. |

| Payment | Deposit of 5-10% is paid into escrow. | The remaining balance of the sale price and all fees are paid. |

Getting to grips with this notaire-led process is the key to a smooth and secure purchase in France. The system is built on legal certainty, ensuring that when you finally turn that key in the door, the property is well and truly yours.

Getting to the Finish Line: Closing the Deal and Managing Costs

You’ve made it through the offers and waded through the initial paperwork. The finish line is finally in sight. This last leg of the journey is all about dotting the i's and crossing the t's on the finances and completing the final checks before those coveted keys are in your hand.

The Waiting Game

The period between signing the Compromis de Vente and the final Acte de Vente can feel like a nail-biting wait, typically lasting two to three months. Don't worry, this quiet spell is productive. Behind the scenes, the notaire is meticulously combing through land registries and legal documents to ensure the property title is clean and clear for transfer.

For you, the buyer, the primary mission during this time is simple but crucial: get your money ready for the big day.

Getting the Funds in Place for the Final Signature

About a week or two before the final signing, the notaire will send you a detailed breakdown of costs, called a décompte. This isn't just a simple invoice; it’s a comprehensive statement that spells out the exact amount you need to wire. It will include the remaining balance on the house, all the various fees and taxes, and any pro-rated property taxes for the year.

This money needs to be transferred directly into the notaire's secure escrow account, known as the compte séquestre. My advice? Don't leave this to the last minute. The funds must be received and cleared before you sit down to sign. An international wire transfer can sometimes hit unexpected delays, and a late payment can push back your closing date. It's always better to send it a few days earlier than you think you need to.

Understanding the True Cost of Buying in France

One of the most common surprises for foreign buyers is realizing the final price is quite a bit higher than the number on the sale agreement. These additional costs, known as closing costs, are a standard part of the process, and budgeting for them from the start will save you a world of stress.

As a rule of thumb, expect your total transaction costs to add 7% to 10% on top of the purchase price for an existing home. So for a €300,000 property, you’ll need to have an extra €21,000 to €30,000 ready to cover all the associated fees.

This chunk of money covers a host of mandatory charges, all of which are managed and disbursed by the notaire. Let's peel back the layers on what these costs, collectively called the frais d'acquisition (or more commonly, frais de notaire), actually cover.

A Detailed Breakdown of Your Closing Costs

People often refer to the entire sum as "notary fees," but the notaire's actual take-home pay is just a small slice of the pie. The vast majority of the money is actually taxes and duties they are required to collect for the French government.

Here’s a look at where your money is going:

- Property Transfer Tax (Droits de Mutation): This is the big one. It's a collection of local and state taxes that makes up the bulk of your closing costs, typically totaling around 5.8% of the property’s price across most of France.

- The Notaire's Official Fee (Émoluments): This is what the notaire earns for their legal work. It’s not a simple percentage but is fixed by the government on a sliding scale based on the property's value.

- Administrative Costs (Débours): Think of this as the notaire getting reimbursed for expenses. They pay out-of-pocket for things like land registry searches, urban planning certificates, and other necessary documents, and you pay them back through these fees.

- Land Registry Fees (Contribution de Sécurité Immobilière): A small but mandatory fee of 0.10% of the property price, paid to officially register you as the new owner.

Don't forget the estate agent's commission if you used one. While it's usually paid by the seller, that cost is almost always baked into the property's asking price from the very beginning.

The Big Day: Signing the Acte de Vente

With the money safely in the notaire's account and all the legal checks cleared, it's time for the final meeting. You'll join the seller at the notaire's office for a somewhat formal ceremony where the notaire reads the entire Acte de Vente aloud. It can be a long document, but it’s done to ensure everyone is fully aware of what they are signing.

Once the reading is complete and everyone has confirmed their understanding and agreement, you’ll sign the deed. The moment your signature hits the paper, the property is officially yours. The notaire will hand over the keys and provide you with an attestation de propriété—a temporary certificate of ownership. The fully registered, official deed will follow from the land registry a few months later.

Congratulations, you are now the proud owner of a home in France

Got Questions About Buying a House in France?

Jumping into the French property market for the first time is exciting, but it naturally brings up a lot of questions. The process has its own quirks, and a small detail can make a big difference down the line. Let's tackle some of the most common things people ask.

Can I Still Buy a House in France After Brexit?

Yes, absolutely. Who can own property in France has nothing to do with nationality. Whether you're from the UK, the US, or anywhere else outside the EU, the laws on property ownership are the same for everyone.

The real change after Brexit isn't about buying; it's about staying. Owning a house doesn't automatically give you the right to live here full-time. You'll still need to navigate the visa and residency permit process if you plan on staying longer than 90 days in any 180-day period.

Do I Really Need a French Bank Account?

Legally, you don't need one just to transfer the purchase funds—that money goes directly to the notaire. But from a practical standpoint, it's a must-have. I always advise clients to open one as soon as they can.

Once the house is yours, you'll have ongoing bills to pay, and a local account makes everything infinitely easier. Think about it:

- Setting up direct debits for electricity, water, and internet.

- Paying your annual property taxes (taxe foncière).

- Handling payments for home insurance or a garden maintenance contract.

Getting an account set up early smooths out all these little life-admin tasks from day one.

What Kind of Property Taxes Should I Expect to Pay Every Year?

Once you're a homeowner, there are two main annual taxes you need to budget for. Forgetting these can be a costly surprise.

- Taxe Foncière: This is the big one—the land and property tax. It's paid by whoever owns the property on January 1st of the tax year. The amount can vary wildly depending on the home's size and condition, but the biggest factor is its location. A village in the Creuse will be a world away from a city like Nice.

- Taxe d'Habitation: This is a residency tax. While the government has phased it out for primary homes, it still applies to all second homes. The amount is set by the local council (commune) based on the property's estimated rental value.

A classic mistake is to underestimate these ongoing costs. Always, always ask the estate agent or the notaire for the previous owner's tax bills. It’s the only way to get a realistic picture of what you'll be paying each year.

How Much Extra Should I Budget for Closing Costs?

It's easy to fixate on the asking price, but the closing costs—what the French call frais d'acquisition or frais de notaire—are a significant chunk of the total. For an existing home (which is most of them), a good rule of thumb is to budget an extra 7-8% on top of the purchase price.

So, on a house listed for €250,000, you're looking at around €17,500 to €20,000 in additional fees. This lump sum covers the property transfer tax, the notaire's regulated fee, and various administrative costs. If you're buying a brand-new build, these costs are much lower, usually just 2-3%.

Ready to turn your French property dream into a reality? At Residaro, we specialize in connecting international buyers with their ideal homes across France. Explore our extensive listings and find your perfect match today. Visit us at https://residaro.com to start your search.