What Is Property Transfer Tax A Homebuyer's Guide

Whenever a property changes hands, there's a good chance a property transfer tax will be part of the deal. Think of it as a one-time government fee charged when the title, or legal ownership, officially moves from the seller to the buyer.

It’s not the same as the annual property taxes you pay. This is a single charge, typically paid at closing, that serves as the government's stamp of approval on the transaction. The revenue it generates goes directly into funding the public services we all rely on.

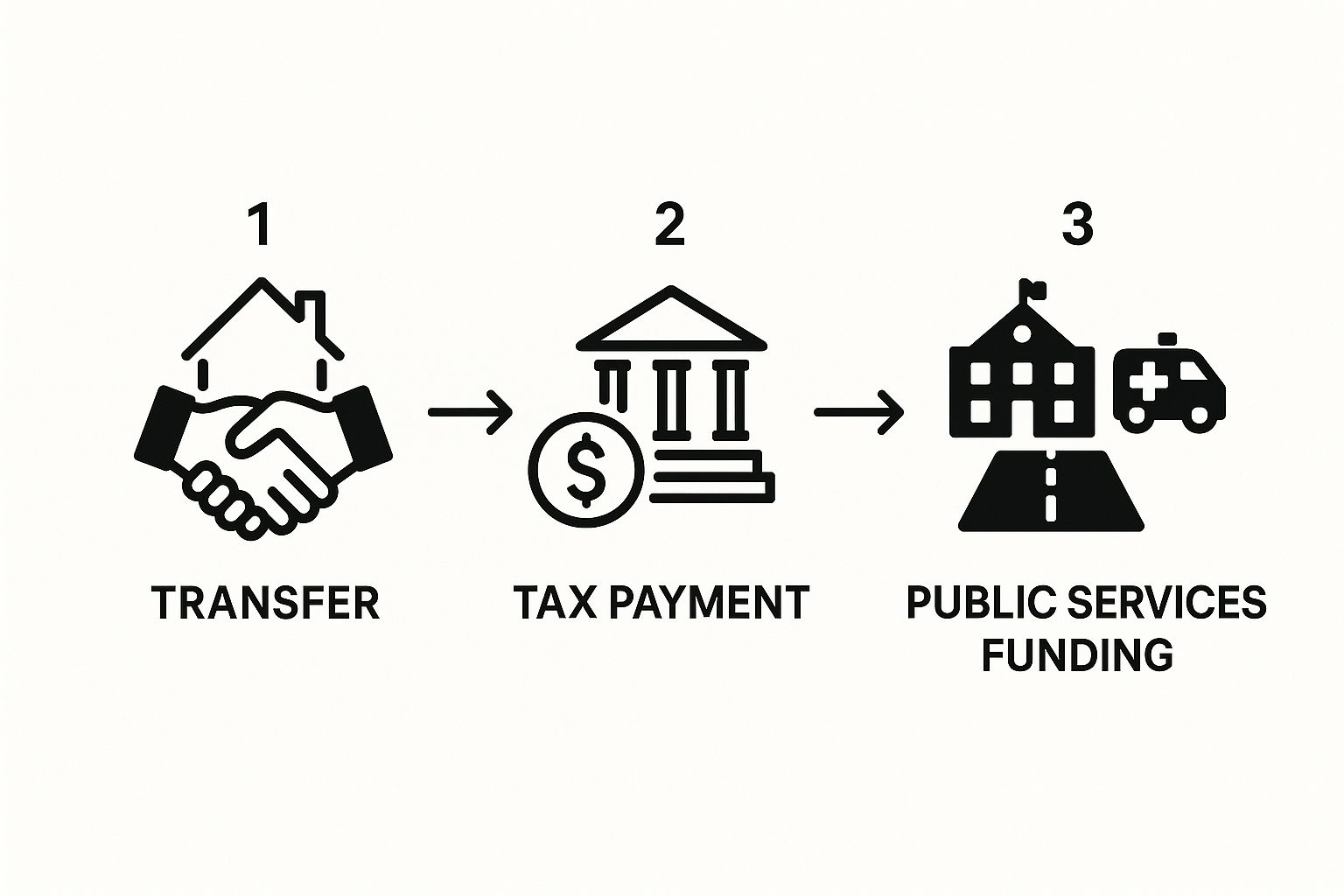

This tax essentially turns a private real estate deal into a source of public good. The infographic below illustrates this process perfectly—showing how the tax collected from a title transfer helps pay for things like new roads, schools, and parks.

As you can see, the tax acts as a vital link, converting the value of a property sale into tangible benefits for the entire community.

Who Are the Key Players?

So, who's actually involved in this? It really boils down to three parties: the buyer, the seller, and the government agency that collects the tax.

- The Buyer: In most cases, the buyer is on the hook for paying the transfer tax when the sale closes.

- The Seller: Sometimes, as part of negotiations, the seller might agree to cover a portion or even all of the tax as a sales concession.

- The Government: This is the entity—whether it’s the city, county, or state—that levies and collects the funds.

This practice isn't just local; it's a standard part of real estate transactions worldwide, though the specifics can change dramatically from one country to the next. For example, some high-value properties in Belgium face a transfer tax as high as 11.3%, while Spain can reach up to 8.0%. Germany, on the other hand, tends to have lower rates, showcasing how different governments approach this.

To get a clearer picture, let's break down the fundamentals.

Property Transfer Tax at a Glance

This table simplifies the core components of the property transfer tax.

| Key Aspect | Explanation |

|---|---|

| What Is It? | A one-time tax on the transfer of property ownership from seller to buyer. |

| Who Pays? | Usually the buyer, but it's often a point of negotiation during the sale. |

| When Is It Paid? | At closing, when the property title is officially transferred. |

| Why Does It Exist? | To generate revenue for local and state governments to fund public services. |

This tax is a foundational piece of how local governments operate, ensuring that real estate transactions contribute to the community's well-being.

Why Does This Tax Exist?

At its heart, the property transfer tax is a straightforward way for governments to raise money. But it also serves another important function: it ensures that the public record of who owns what property is meticulously kept up-to-date. Every time a property is sold and the tax is paid, the transfer is officially recorded, maintaining a clear and accurate chain of title.

For anyone looking to buy property outside their home country, getting a handle on these taxes is absolutely critical. They can add a significant amount to your final purchase price, so factoring them in from the start is essential. If you're navigating this process, it helps to learn more about the complexities of foreign real estate tax.

How Your Property Transfer Tax Is Calculated

Knowing a property transfer tax exists is one thing, but the question every buyer really wants answered is: how much is this actually going to set me back? Thankfully, it’s not some hidden mystery. The calculation is a straightforward formula based on the property’s value.

Most of the time, this value is simply the purchase price you and the seller agreed on. However, in some cases, like if the property is a gift, the government will use its fair market value to calculate the tax instead.

Governments generally stick to one of two methods to figure out the final tax bill: a simple flat percentage or a more nuanced tiered system. Which one your chosen region uses will directly affect your closing costs, so it’s crucial to know what to expect.

What Is the Tax Actually Based On?

Before we jump into the math, we need to understand the number the tax is calculated from. This is often called the taxable consideration.

While it's usually the cash you're paying, "consideration" can include other forms of value. For example, if you agree to take over the seller’s remaining mortgage as part of the purchase, that debt could be added to your cash payment to determine the total consideration. This is a critical detail, as it can bump up the taxable amount and lead to a bigger tax bill than you initially budgeted for.

Flat Rate Calculations: The Simple Approach

The most direct way authorities calculate property transfer tax is with a flat rate. This method is exactly what it sounds like—a single, fixed percentage is applied to the property's entire value, no matter the price. It's predictable and super easy to figure out.

Let’s say a city charges a flat transfer tax of 1.5%.

Example Calculation:

- Property Purchase Price: $500,000

- Flat Tax Rate: 1.5% (which is 0.015)

- Tax Owed: $500,000 x 0.015 = $7,500

In this scenario, your tax is a clean $7,500. No complicated brackets or tiers to navigate—just simple math.

Tiered Rate Calculations: A Progressive Model

A tiered, or progressive, system is a bit more involved. Here, the tax rate actually increases as the property's value goes up. Instead of a single flat rate, different percentages apply to different portions of the property's value. Think of it like income tax brackets. The idea is to ease the tax burden on less expensive homes.

Let's run the numbers for the same $500,000 property, but this time with a tiered system in place.

- 1% on the first $200,000 of value

- 2% on the portion from $200,001 up to $400,000

- 2.5% on the remaining value above $400,000

To get our total, we have to calculate the tax for each "slice" of the value and then add them all together.

- First Tier: 1% of $200,000 = $2,000

- Second Tier: 2% of the next $200,000 ($400,000 - $200,000) = $4,000

- Third Tier: 2.5% of the final $100,000 ($500,000 - $400,000) = $2,500

Total Tax Owed (Tiered): $2,000 + $4,000 + $2,500 = $8,500

As you can see, the final bill is higher under this specific tiered structure. It's also vital to remember that property transfer tax is just one piece of the puzzle. To get the complete picture of your financial responsibilities, especially with international real estate, you should also understand the rules around capital gains tax on foreign property, which comes into play when you decide to sell.

Comparing Transfer Tax Rates Around The World

If you think property transfer tax is a simple, standard fee, think again. The moment you look beyond your local market, you’ll discover it’s a fascinating mosaic of different economic strategies and government priorities. What one country considers a vital revenue stream, another might see as a major roadblock to attracting new investment.

This isn't random. These variations are a direct reflection of a region's goals. A country trying to cool down a red-hot real estate market might slap on a higher tax to curb speculation. On the other hand, a nation eager for foreign capital will often keep its rates appealingly low to roll out the welcome mat for international buyers.

For anyone even thinking about buying property abroad, getting a handle on these differences is crucial. This single tax can swing from a minor closing fee to a massive financial hurdle, potentially making or breaking your entire investment plan.

A Look At Rates Across Different Jurisdictions

To get a real sense of how much this tax can vary, let's take a quick trip around the world. You’ll see that the approach can differ wildly, from nationwide rules to taxes that are specific to a single city.

- United States: There’s no federal property transfer tax here. Instead, you're dealing with a complex patchwork of state, county, and even city-level taxes. Delaware, for instance, charges a hefty 4%, while a city like Philadelphia tacks on its own local tax on top of the state’s cut.

- Canada: Much like its southern neighbor, transfer taxes in Canada are handled by the provinces. British Columbia uses a tiered system that can climb to 3% on high-value homes, and if you're buying in Toronto, get ready to pay both a provincial tax and a substantial municipal one.

- United Kingdom: In England and Northern Ireland, they use a progressive system called Stamp Duty Land Tax (SDLT). The rate climbs with the property's price tag, starting at 0% for the cheapest homes and jumping to 12% for the most expensive portions.

- European Union: It's a mixed bag across the EU. Belgium stands out with rates that can soar past 10%. Meanwhile, popular destinations like Portugal and Spain use tiered systems that usually land somewhere between 6% and 8%.

This just goes to show why you absolutely have to do your homework on the specific rules for the exact location you plan to buy in.

Why Do These Rates Vary So Much?

So, what's behind these wildly different numbers? It often comes down to a government's economic philosophy and its immediate needs. If a local government is facing a budget shortfall, a real estate transaction looks like a pretty good opportunity to raise funds without touching more politically charged areas like income or sales tax.

For example, Switzerland generally keeps its rates low—typically between 1% and 3% depending on the canton—which helps maintain a stable and attractive market. Bulgaria is even lower, with a tax that ranges from just 0.1% to 3%. In stark contrast, the European Union as a whole raked in a massive €318.8 billion in property tax revenues in 2023, which shows just how critical this funding is for public services across the continent. You can discover more insights about European property tax collection and see how different countries stack up.

This strategic use of tax policy gives governments a powerful lever to fine-tune their housing markets. By making transactions more or less expensive, they can encourage or discourage buying activity to meet their larger economic goals.

Comparative Property Transfer Tax Rates by Country

Seeing the numbers side-by-side really drives home just how much the tax landscape can change from one border to the next. The table below gives a snapshot of what you might expect to pay in various countries, offering a clear comparison for anyone looking to buy internationally.

| Country / Region | Typical Transfer Tax Rate Range | Key Considerations |

|---|---|---|

| USA (Varies by State) | 0% - 4%+ | No federal tax; rates are set at state, county, or city levels. |

| Canada (Varies by Province) | 0.5% - 3%+ | Provincial tax is standard; major cities may add a municipal tax. |

| United Kingdom | Progressive, up to 12% | Uses a tiered system (Stamp Duty) with higher rates for higher values. |

| Spain | 6% - 10% | Varies by autonomous region; generally a significant closing cost. |

| Portugal | Up to 8% | A progressive tax (IMT) based on the property's value and type. |

| Germany | 3.5% - 6.5% | Set at the state level (Grunderwerbsteuer), varying between federal states. |

As this table makes clear, understanding what is property transfer tax in one country gives you almost no clue what to expect in another. Getting this global perspective is the first step toward building a realistic budget for an overseas property investment and, most importantly, avoiding nasty financial surprises when it's time to sign the papers.

How Transfer Taxes Shape the Housing Market

The property transfer tax isn’t just some minor fee buried in your closing documents—it’s a powerful lever that can significantly influence the entire real estate market. Think of it as a toll on the property highway. A low toll encourages a steady flow of traffic, but a high one can cause a serious jam, making people think twice before getting on the road.

This tax has a direct impact on everything from buyer behavior and property values to how often people are willing to move. A hefty transfer tax inflates the total cost of buying a home, which can easily push potential buyers to the sidelines and cool down demand. This isn't just a theory; it's a real-world economic effect that dictates the health and energy of a local housing market.

The Impact on Market Activity and Mobility

One of the most immediate consequences of a high property transfer tax is a noticeable slowdown in real estate activity. When the cost of moving becomes prohibitively expensive, homeowners often decide to stay put, even if their current home no longer fits their needs. This is what economists call the "lock-in effect," and it throws a wrench into the natural churn of the market.

This has real consequences for people and the economy. A growing family might put off buying a larger home, or an empty nester could delay downsizing—all to sidestep a massive tax bill. This friction also makes it harder for people to relocate for a new job, which can stifle career growth and the broader economy.

A higher tax essentially acts as a penalty on moving. This can lead to a less efficient housing market where properties are not allocated to those who need them most, simply because the transaction costs are too prohibitive.

This slowdown isn't just about buyers and sellers. When fewer homes are changing hands, it means less business for everyone in the industry, from real estate agents and mortgage brokers to movers and renovation contractors.

How Tax Rates Influence Property Values

The link between transfer taxes and property values is a delicate one. While the tax is designed to raise public funds, it can ironically suppress the very home values it’s based on. When buyers know they need to set aside an extra few percent for taxes, they naturally adjust their budget for the house itself.

This means they’ll likely offer less for the property to offset the higher closing costs, creating downward pressure on home prices. The effect is well-documented. Research summarized by BOMA International shows that a 1% increase in the transfer tax can cause property values to drop by about 1% and the number of sales to fall by a staggering 8%. These figures really highlight how sensitive the market is to tax policy changes.

This is especially true in markets where affordability is already a major concern. Tacking on thousands of dollars in closing costs can be the final straw that puts homeownership just out of reach for many, further dampening demand and, in turn, property values.

The Debate Over Affordability and Revenue

The central conflict with the property transfer tax is its two competing roles. On one hand, it's a crucial source of revenue for essential public services like schools and infrastructure. On the other hand, it can make the housing affordability crisis even worse.

This leaves policymakers walking a tightrope. Raising the tax can bring in much-needed cash, but it risks slowing down the real estate sector—an industry that, in some regions, drives nearly a fifth of the state's entire economic output.

Faced with steep upfront costs, many would-be buyers start to second-guess their plans. This often sparks a critical conversation in many households, and you can explore our guide on https://residaro.com/blog/is-it-cheaper-to-rent-or-buy to see how these costs fit into the bigger financial picture. In the end, striking the right balance between funding public needs and maintaining a healthy, accessible housing market remains one of the toughest challenges for governments everywhere.

Finding Common Tax Exemptions and Reductions

While property transfer tax is a standard part of most real estate deals, it’s not always set in stone. Many governments build in specific exemptions and reductions to support policy goals, like making homeownership more accessible or making it easier to pass property down through a family. Think of these as financial relief valves built right into the tax system.

For you as a buyer, knowing about these potential breaks is incredibly powerful. Not looking into whether you qualify for an exemption is like leaving a pile of cash on the table at closing. These programs can literally save you thousands of dollars—or even wipe out your tax bill entirely—so they’re a critical part of budgeting for a property purchase.

First-Time Homebuyer Programs

One of the most common and valuable breaks is aimed squarely at first-time homebuyers. Governments get it: coming up with a down payment and covering all the closing costs is a massive hurdle for anyone new to the market. To lighten that load, many places offer a partial or even a full waiver of the property transfer tax.

The whole point is to help more people get a foot on the property ladder. Of course, these programs always have strings attached.

- Who is a "First-Time Buyer"? Usually, it means you can’t have owned a residential property anywhere in the world, ever.

- Is There a Price Limit? The tax break might only apply to homes under a certain price cap.

- Do You Have to Live There? You’ll almost certainly need to use the property as your main home for a minimum period.

Forgetting to check for these programs is a classic mistake that can cost new buyers a small fortune.

Breaks for Primary Residences

Even if this isn't your first rodeo, you might still catch a break. Some regions offer lower tax rates when the property you're buying will be your primary residence. The thinking here is to support people buying a home to live in, rather than those buying purely for investment.

This kind of reduction separates buying a home from buying a business asset. For instance, a state might charge a 1% transfer tax on a primary home but bump that up to 2.5% for all other properties, like vacation homes or rental units. It's a clear policy choice to make everyday homeownership just a little more affordable.

These targeted tax reliefs are crucial tools for policymakers. They help stabilize communities by encouraging people to put down roots and ensure the tax burden is fairer based on how the property is actually used.

Transfers Between Family Members

What about when a property changes hands but no money is involved? This happens all the time within families, and thankfully, most tax codes have it covered. Property transfers that happen because of an inheritance, a gift between close relatives, or a divorce settlement are often completely exempt from transfer tax.

Here are a few common scenarios:

- A parent signs the family home over to their child.

- Spouses divide their properties as part of a divorce.

- Someone inherits a house from a deceased relative's estate.

The key detail is that there's usually no "consideration"—or money—being exchanged like in a normal sale. Because it's not a market transaction, governments often waive the tax. You will, however, need to prove the family relationship and the nature of the transfer with documents like birth certificates, marriage licenses, or legal agreements. It’s always smart to check the local rules, as the definition of a "close relative" can differ from one place to another.

Got Questions About Property Transfer Tax? We’ve Got Answers.

Even with a solid grasp of the basics, property transfer tax can feel a bit murky. It's one of those details that tends to get confusing right when you’re trying to navigate one of the biggest purchases of your life. Let's clear the air and tackle some of the most common questions head-on.

Think of this as your quick-reference guide. We'll give you straightforward answers to the practical concerns that almost always pop up during a real estate deal, giving you the clarity you need to move forward with confidence.

Is This the Same Thing as My Annual Property Tax?

This is easily the most frequent point of confusion, and the answer is a hard no. These are two completely separate taxes, each with a different job to do.

Here’s a simple way to think about it: the property transfer tax is like a one-time cover charge you pay to get into a concert. You pay it once for the "event" of the property changing hands.

Your annual property tax, on the other hand, is more like a recurring subscription. It's what you pay every year to your local government for ongoing services that benefit you as a homeowner—things like public schools, road maintenance, and fire departments.

The Bottom Line: Transfer tax is a one-time fee paid at closing to finalize the sale. Annual property tax is a recurring cost of homeownership that you'll pay every single year.

Mixing these two up is a recipe for a budget disaster, so it's vital to account for them separately in your financial planning.

So, Who Actually Pays the Transfer Tax?

In most real estate deals, the buyer is legally on the hook for paying the property transfer tax. It’s generally bundled in with other standard buyer-side closing costs, right alongside things like appraisal fees and title insurance. But this isn't set in stone.

Like a lot of things in a home sale, who pays this tax can become a point of negotiation. If you're in a buyer's market where sellers are eager to make a deal, you might successfully negotiate for the seller to cover some or even all of the transfer tax. On the flip side, in a hot seller's market with bidding wars, you’ll have a much harder time getting a seller to agree to that.

Ultimately, who pays comes down to two things:

- Local custom and law: Some regions have clear rules about which party typically pays.

- The purchase agreement: At the end of the day, what matters is what you and the seller agree to in the final, signed contract.

Always make sure this point is crystal clear during negotiations so there are no last-minute surprises at the closing table.

How and When Does This Tax Get Paid?

The property transfer tax is almost always paid at closing. This is that final meeting where stacks of documents are signed, money changes hands, and the property title is officially transferred from the seller to you.

The whole process is managed by the closing agent—usually an attorney or someone from a title company. They’re responsible for calculating the exact transfer tax you owe based on the home's sale price and the local tax rates. You'll see this amount itemized on your closing disclosure statement, which is the document that breaks down all your final costs.

You'll typically bring a certified check or arrange a wire transfer for the total amount due, which covers the purchase price, other closing costs, and the transfer tax. The closing agent then cuts the check to the right government agency, making sure the tax is paid and the transfer is officially recorded.

Can I Deduct Property Transfer Tax on My Taxes?

This is a huge question for financial planning, but the answer for most people is no, not directly. You can't write off the property transfer tax on your income tax return in the year you buy the house, unlike deductions for mortgage interest or your annual property taxes.

But it’s not a complete loss from a tax standpoint. The IRS does let you add the cost of the property transfer tax to your home's cost basis. The cost basis is essentially the total investment you've made in the property.

Why is that important? Because a higher cost basis can lower your taxable capital gains when you eventually sell the home. For example, if you paid $5,000 in transfer tax, that amount gets added to your original purchase price. This makes your "profit" look smaller on paper, potentially saving you a good chunk of money on capital gains tax down the line. As always, it's a smart move to talk this over with a tax professional who can give you advice for your specific situation.

Ready to find your perfect home in Europe? At Residaro, we simplify the search process, offering a curated selection of beautiful properties in sought-after destinations. Start exploring your dream home today.