How to Buy Property in Portugal - A Complete Guide

Buying property in Portugal is an exciting prospect, but before you get swept away by visions of coastal villas, there are a few essential administrative tasks to tick off. Getting these done first isn't just bureaucracy; it's about building a solid foundation for a smooth and secure purchase.

Let's break down the three non-negotiables: getting your tax number (NIF), opening a bank account, and finding a good independent lawyer.

Laying the Groundwork for Your Property Purchase

Think of these initial steps as your pre-flight checklist. You wouldn't take off without one, and you shouldn't start your property hunt in Portugal without this groundwork in place. Taking care of this now saves you from massive headaches and delays when you find the perfect place.

Get Your Portuguese Tax Number (NIF)

First things first, you need a Número de Identificação Fiscal, better known as a NIF. This unique nine-digit number is your golden ticket for pretty much any official transaction in Portugal. You can't buy a house, open a bank account, or even get a phone contract without it.

Getting a NIF is refreshingly straightforward. You can apply in person at a local Finanças (tax office) or a Loja do Cidadão (citizen's shop). Just bring these two things:

- Your passport or another valid government-issued ID.

- Proof of address from your home country (a recent utility bill or bank statement works perfectly).

If you're a non-EU/EEA resident, you’ll need a fiscal representative in Portugal to handle the application. Don't worry, this is standard practice. Many law firms and specialized agencies offer this service for a small fee, which allows you to get it all done remotely before you even arrive. It’s money well spent for the convenience.

Open a Portuguese Bank Account

With your shiny new NIF in hand, the next logical step is opening a local bank account. This is absolutely essential. All the money for your deposit and the final purchase will need to flow through this account. It also makes life infinitely easier later for paying property taxes, utilities, and any condo fees.

The process is simple: walk into a bank with your NIF, passport, and proof of address. Having a local account streamlines the whole financial side of things, especially when you're transferring large sums or setting up a mortgage. Major banks in cities and popular expat areas like the Algarve are well-versed in dealing with international clients and almost always have English-speaking staff.

Hire an Independent Property Lawyer

I can't stress this enough: this is the most important decision you will make. Your real estate agent's job is to serve the seller's interests. Your lawyer’s job is to protect yours. They are your advocate, your advisor, and your safety net.

Your lawyer is the one who does the deep dive into the property's paperwork. They check for outstanding debts, ensure the seller actually has the legal right to sell, and confirm there are no nasty surprises hiding in the property's history. Trying to save money by skipping this step is one of the biggest and most costly mistakes international buyers make.

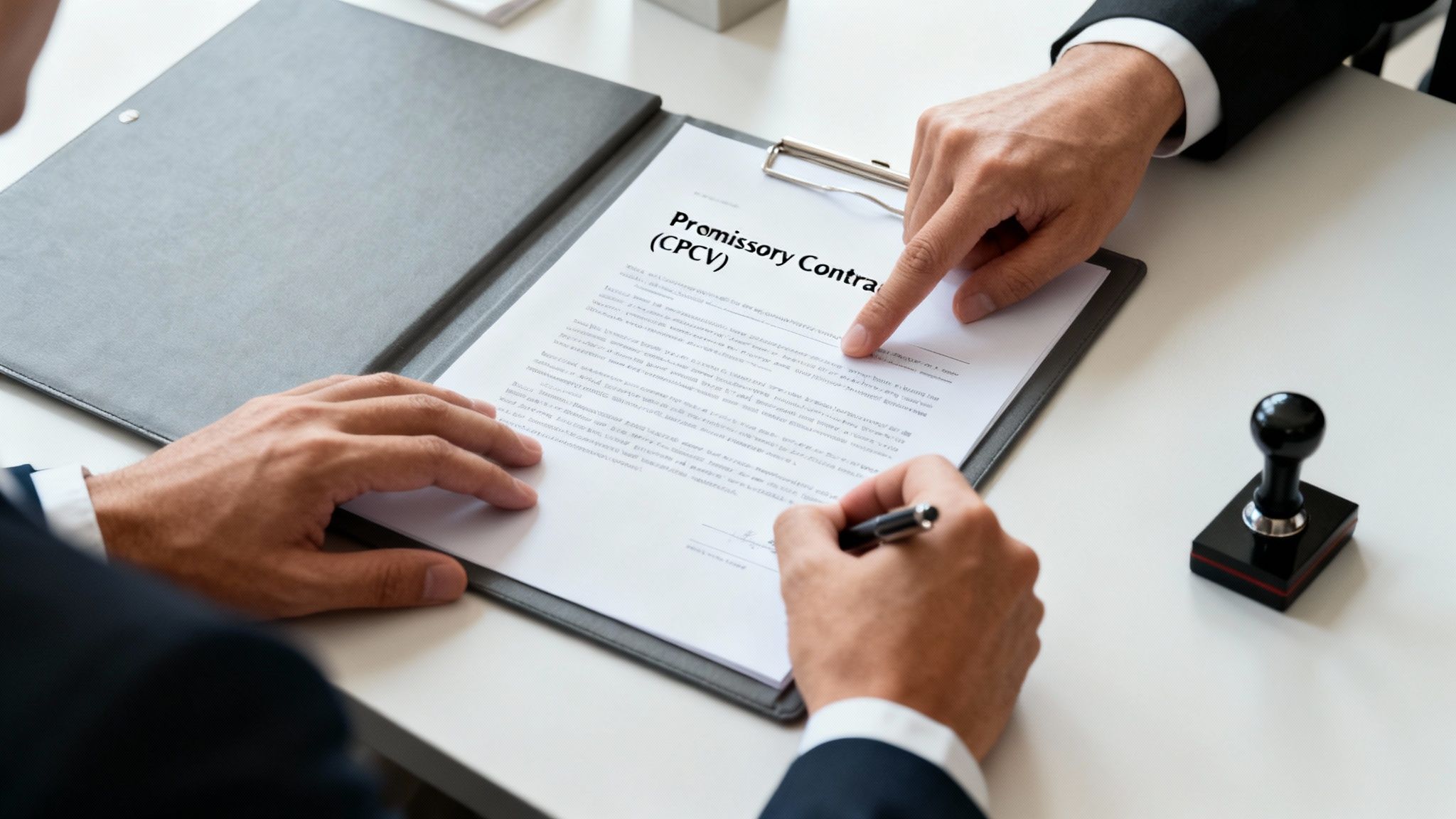

A great lawyer will guide you through everything, from reviewing the promissory contract (Contrato de Promessa de Compra e Venda - CPCV) to representing you at the final signing. Their expertise is invaluable. Expect to pay somewhere between €1,000 and €2,000 for their services—a tiny price for complete peace of mind.

To help you get started, here’s a quick summary of these first steps and what you can expect to budget for them.

Your Initial Buyer Checklist and Estimated Costs

| Action Item | Why It's Essential | Estimated Cost |

|---|---|---|

| Get a NIF Number | Required for all financial and legal transactions in Portugal. You can't open a bank account or sign a contract without it. | Free if done in person; €100 - €200 if using a fiscal representative. |

| Open a Local Bank Account | Needed to transfer funds for the purchase, pay taxes, and handle ongoing property-related expenses. | Free to open, but some banks may have small monthly maintenance fees. |

| Hire an Independent Lawyer | Your legal protection. They perform due diligence, review all contracts, and ensure the transaction is secure and legitimate. | €1,000 - €2,000+ (often a percentage of the property value, with a minimum fee). |

Getting these three items sorted out is a low-cost but high-impact way to start your property journey on the right foot. Once you have this foundation, you'll be in a much better position to tackle the bigger picture of financing and closing costs, which other Portuguese real estate experts explore in more detail.

Finding Your Perfect Home in Portugal

Alright, with your NIF, bank account, and lawyer sorted, it's time for the fun part: the actual property hunt. This is where the dream starts feeling real—whether you're picturing a sun-drenched apartment in the Algarve, a rustic quinta in the countryside, or a chic Lisbon flat.

The Portuguese property market is buzzing with opportunities, but you need to know where to look. I've found that the best approach is a blend—kicking things off with powerful online tools and then pairing that with the boots-on-the-ground expertise of a local agent. This combo gives you a serious advantage.

Starting the Search Online

The modern property search almost always begins online, and for good reason. It’s the best way to get a solid feel for what’s out there without leaving your couch. You can browse thousands of listings, get a handle on prices, and see the different styles of homes across the country.

Online portals have powerful filters that let you really drill down on what you want. You can typically narrow your search by:

- Location: Zero in on a specific city like Porto or an entire region like the Silver Coast.

- Property Type: Easily filter for apartments (apartamentos), houses (moradias), or even plots of land (terrenos).

- Price Range: This is essential. Set your budget and stick to it to avoid temptation.

- Key Features: Got to have a pool? A sea view? A certain number of bedrooms? Just tick the boxes.

Using these filters effectively lets you build a solid shortlist of properties that actually meet your criteria. This saves an incredible amount of time before you even think about booking viewings.

An online search is your reconnaissance mission. It gives you a fantastic overview of market values and helps you define your absolute must-haves. But it rarely tells the whole story. Use it as a launchpad, not the final word.

Why You Need a Good Local Agent

While portals are great for casting a wide net, nothing beats the insider knowledge of a local real estate agent, or imobiliária. A great agent does so much more than just unlock doors. They're your guide, offering priceless context on different neighbourhoods, navigating local market quirks, and often giving you a heads-up on off-market properties that you'd otherwise never see.

An experienced local agent will take the time to understand your vision and help you navigate a market that's seen some serious growth. For instance, the average house price per square meter recently hit a record €2,065, a 19% jump year-on-year. While hotspots like Greater Lisbon reached €3,403/m², some savvy investors are looking at emerging regions like Baixo Alentejo, where prices shot up by a staggering 38.7%. That kind of insight is invaluable.

Understanding the Different Markets and Locations

Portugal’s regions are incredibly diverse, each offering a unique lifestyle and investment profile. Where you buy really depends on what you're looking for.

- Love the City Buzz? Lisbon and Porto are the obvious choices. They're packed with culture, have strong rental demand, and offer everything from historic apartments to modern new-builds.

- Chasing the Sun? The Algarve is the classic destination for holiday homes and retirees. It's famous for its world-class beaches, golf courses, and large, well-established expat communities.

- Wanting Authentic Charm? Head to the Silver Coast or explore central Portugal. Here you’ll find more traditional towns, a much slower pace of life, and generally more affordable property prices.

Doing a bit of research into these different markets is crucial. It helps you align your property search with your long-term goals. For a deeper dive, check out our comprehensive guide on Portugal house prices to see exactly how the regions stack up. Being well-informed is the key to making a smart investment.

Navigating the Legal Journey to Ownership

So, your offer has been accepted. Congratulations! Now the real work begins. This is where the process shifts from house-hunting to the nitty-gritty legal details that will officially make the property yours. It might seem daunting, but it's a well-trodden path designed to protect both you and the seller. With a good lawyer by your side, you'll move through a few key milestones: the promissory contract, a deep dive into due diligence, and finally, signing the deed.

The Promissory Contract: Your Binding Agreement

The first major legal step is signing the Contrato de Promessa de Compra e Venda (CPCV), what we call the promissory contract. Don't mistake this for a simple letter of intent; this is a serious, legally binding agreement that locks in the sale. It’s the moment everyone formally commits to the deal.

When you sign the CPCV, you'll transfer a deposit, usually between 10% and 20% of the purchase price. This shows you're a serious buyer. Your lawyer will draft this contract with incredible care, making sure every single detail of the sale is laid out in black and white.

Make sure the CPCV explicitly states:

- The final purchase price and the exact deposit amount.

- A detailed description of the property that perfectly matches what's on the official records.

- A firm deadline for signing the final deed (Escritura).

- Any "out" clauses or conditions that need to be met, like the seller completing a small repair or you securing your mortgage approval.

This contract has real teeth. If you, the buyer, decide to walk away after signing, you’ll almost certainly lose your deposit. On the flip side, if the seller backs out, Portuguese law requires them to pay you back double the deposit as a penalty. It’s a powerful protection for buyers.

The Crucial Due Diligence Phase

While the CPCV is being drawn up, your lawyer should be hard at work on due diligence. This is the detective work—the background check on the property itself. It's an absolutely essential safety net to ensure you aren't buying a property with hidden debts, illegal construction, or other nasty surprises.

Your lawyer's investigation will cover a lot of ground. They'll confirm the seller is the true legal owner and has the right to sell. They’ll also pull records from the Land Registry (Conservatória de Registo Predial) and the local tax office (Finanças) to verify the property’s size, boundaries, and most importantly, to check for any outstanding mortgages, liens, or unpaid taxes tied to it.

One of the biggest deal-breakers we see is an issue with the habitation license, or Licença de Utilização. This document proves the property was built legally and is certified for residential use. Without it, you can't get a mortgage, and you can't legally complete the purchase. It's a non-negotiable.

I’ve seen this trip up buyers time and time again. For instance, someone finds a charming old farmhouse built before 1951, which often exempts it from needing a license. What they don't realise is that a beautiful new pool and annex were added in the 90s without any permits. That makes a portion of the property illegal, and it becomes a nightmare to sell or finance until it's legalized—a process that can take years and cost a fortune. A sharp lawyer will catch this instantly.

Signing the Final Deed and Taking Ownership

The grand finale of your legal journey is signing the Escritura Pública de Compra e Venda—the Final Deed. This is the official ceremony where the property ownership is legally transferred to you. It happens at a notary's office with you, the seller, and your respective legal reps all present.

Before you get to this stage, you'll need to have transferred the remaining balance of the purchase price, plus funds for taxes, into your Portuguese bank account. At the meeting, the notary will read the entire deed aloud to ensure everyone understands and agrees. Once all the details are confirmed, the signatures go down. This is also when you'll pay the property transfer tax (IMT) and Stamp Duty.

With the ink dry, the deal is done. The notary handles the official registration, and within a few weeks, the Land Registry is updated to show you as the new legal owner. You’ll get a copy of the deed, and more importantly, the keys to your new home in Portugal. Welcome

Budgeting for Your Total Purchase Cost

That exhilarating moment when your offer gets accepted is one to celebrate. But it's also the cue to shift your focus from the sticker price to the total cost of acquiring your new home. The number on the purchase agreement is just the beginning. In Portugal, a series of taxes and fees come into play before the keys are officially yours.

Forgetting to budget for these is a rookie mistake that can cause a world of financial stress right at the finish line. A solid rule of thumb? Set aside an extra 8% to 10% of the property's purchase price. This buffer is your safety net, ensuring you're not scrambling for cash when it's time to close.

The Big One: IMT (Property Transfer Tax)

The largest chunk of your closing costs will almost certainly be the Imposto Municipal sobre Transmissões Onerosas de Imóveis, or IMT. Think of this as the main tax you pay when a property changes hands. Crucially, you have to pay the IMT before you sign the final deed. The notary can't and won't proceed without proof of payment.

IMT isn't a flat tax; it’s calculated on a progressive scale. The higher the property value, the higher the tax rate. The rates also change depending on whether the property is your primary home or a second home/vacation property.

For instance, a primary residence bought for €250,000 will have a lower IMT bill than a holiday apartment of the same value. Your lawyer will handle the precise calculation, so you know exactly what you owe before the final signing day.

Stamp Duty and Other Essential Fees

Next on the list is Stamp Duty, or Imposto do Selo. This is a much simpler, flat-rate tax applied to official documents and contracts, including property deeds.

Stamp Duty is a fixed 0.8% of the property’s declared value. If you're getting a mortgage from a Portuguese bank, there's an additional Stamp Duty of 0.6% on the loan amount.

Beyond taxes, you’ll also cover the professional services that make the transaction legally binding. This includes:

- Notary Fees: The notary is a neutral, state-appointed official who verifies everyone's identity and ensures the deed is executed legally.

- Land Registry Fees: After signing, your ownership must be recorded at the Land Registry (Conservatória de Registo Predial). This fee covers the administrative work of updating the official property records.

Combined, the notary and registration fees usually add up to about 1% to 2% of the purchase price.

To help you visualize these costs, here’s a quick breakdown.

Breakdown of Property Purchase Taxes and Fees

This table provides an estimated look at the one-off costs you'll face when buying property in Portugal. It’s a great starting point for building a realistic budget.

| Cost Component | What It Is | Estimated Percentage/Cost |

|---|---|---|

| IMT (Property Transfer Tax) | The main tax on property ownership transfer. | Variable (up to 7.5%), based on property value, type, and location. |

| Stamp Duty (Imposto do Selo) | A fixed-rate tax on the deed and other official documents. | 0.8% of the property value. |

| Mortgage Stamp Duty | An additional Stamp Duty if you take out a mortgage in Portugal. | 0.6% of the loan value. |

| Notary & Registration Fees | Fees for the notary's services and officially registering the property in your name. | 1% - 2% of the property value. |

| Legal Fees | The cost for your lawyer to conduct due diligence and manage the transaction. | Typically 1% - 2% of the property value. |

Remember, these are estimates. Your lawyer will provide the exact figures for your specific purchase, but this gives you a clear picture of what to expect.

Don't Forget the Annual Taxes

Your financial planning shouldn't stop at closing. As a property owner in Portugal, you'll have an annual municipal tax to pay called Imposto Municipal sobre Imóveis (IMI).

IMI is calculated using the property's registered tax value (the Valor Patrimonial Tributário or VPT) and a rate set by the local municipality, which usually lands between 0.3% and 0.45% for city properties. To get the full picture of this and other ongoing expenses, dive into our detailed guide on property taxes in Portugal. Knowing these long-term costs is key to understanding the true cost of your investment.

Financing Your Purchase and Thinking About Residency

Finding your dream home in Portugal is a huge milestone, but two big questions usually pop up right around the same time: "How will I pay for this?" and "Could I actually live here?" Figuring out the mortgage landscape and your residency options are the next crucial steps in making your Portuguese dream a reality.

Let's start with the money. The good news is that getting a mortgage in Portugal as a non-resident is very common. The local banks are well-versed in working with international buyers, but you should expect the terms to be a bit different from what a Portuguese citizen might get.

Getting a Mortgage in Portugal

The biggest difference you'll see as a non-resident is the Loan-to-Value (LTV) ratio. A local buyer might get a mortgage covering 80% or even 90% of the home's price. For international buyers, however, that figure is usually closer to 60% to 70%.

What does this mean for you? It means you'll need to prepare for a larger down payment—at least 30% of the purchase price, plus enough to cover all the associated taxes and fees we discussed earlier.

The application itself is pretty standard, but Portuguese banks are meticulous. They’ll want a complete picture of your financial health. Start gathering your documents early, as you'll almost certainly need:

- Proof of income: Recent payslips and tax returns from the past couple of years.

- Bank statements: Typically the last six months from your primary bank back home.

- Credit report: A copy of your credit history from your home country.

- Portuguese details: Your NIF number and the details of your new Portuguese bank account.

- The Promissory Contract (CPCV): A copy of the initial sales agreement for the property.

I always recommend getting pre-approved for a mortgage before you even make an offer. It gives you a rock-solid budget, so you know exactly what you can afford. More importantly, it shows sellers you’re a serious buyer, which can give you a real edge during negotiations.

Expert Tip: Should you use a Portuguese bank or one from back home? A local Portuguese bank is often the path of least resistance because they know the system inside and out. However, if you have a strong relationship with your bank at home and they offer international property loans, you might find a more competitive interest rate. It's always worth exploring both options.

Your Path to Portuguese Residency

For many, buying a property is the first concrete step toward spending much more time in Portugal—or even moving here for good. While owning a home doesn't automatically grant you residency rights, it plays a vital role in many visa applications.

The popular Golden Visa program recently changed, and real estate investment is no longer a direct route to residency. Because of this, many people are now looking at other avenues, with the D7 Visa being one of the most common.

The D7 Visa is often called the "passive income visa" because it's designed for non-EU citizens with a steady, reliable income from sources like pensions, investments, or rental properties. Your newly purchased home can be used as proof of accommodation—a critical requirement for the D7 application. It's a fantastic option for retirees or anyone who is financially independent.

To get a full breakdown of the process, you can learn more about how to get residency in Portugal in our detailed guide. It will walk you through the various requirements and help you figure out the best visa for your specific situation.

Dodging the Bullets: Common Pitfalls for International Buyers

Look, buying property in Portugal is a dream for many, but learning from the mistakes of others is the smartest way to make sure it doesn't turn into a nightmare. The process here is solid and secure, but a few common missteps can cost you dearly.

When you find that perfect villa with the ocean view, the excitement can be overwhelming. It's easy to get swept up and rush through the process, but that’s precisely when the most expensive errors are made. Let's talk about the biggest ones we see time and time again.

Going Without Your Own Lawyer

This is, without a doubt, the number one mistake. It might seem easier or cheaper to use the lawyer suggested by the seller or their real estate agent, but this is a massive conflict of interest.

Remember this: the agent works for the seller. Their goal is to close the deal. Your lawyer works for you. Their only job is to protect your interests, and that means digging into the nitty-gritty legal details you wouldn’t even know to look for.

A good, independent lawyer will verify that the property is free of outstanding debts or mortgages. Why does this matter so much? Because in Portugal, debts can be tied to the property, not the person. If you buy a house with the previous owner's unpaid mortgage or utility bills, that debt could legally become yours. This single check can save you from a financial disaster.

Not Understanding What the Land is For

Here’s another classic trip-up: land classification. You stumble upon a stunning, cheap plot of land and start picturing your dream home. But then you find out it's classified as rústico (rustic) and not urbano (urban).

This distinction changes everything.

- Rustic Land (rústico): This is land meant for farming, forestry, or conservation. Getting permission to build a new house on it is next to impossible.

- Urban Land (urbano): This is land zoned for construction. It’s what you need if you want to build.

Countless buyers have been heartbroken after purchasing a beautiful piece of rustic land, only to have their building plans completely shot down by local zoning laws. Your lawyer is the one who will check the official municipal plan, the Plano Diretor Municipal (PDM), to make sure the property you're buying can actually be used for what you intend.

A cautionary tale we see all too often involves properties with "illegal" extras—think of a swimming pool or a small guest annex that was built without a permit. If these structures aren't properly licensed, the local council (câmara) has the power to order you to tear them down. Even worse, you won't be able to legally sell the property until you fix the problem. This is exactly what a thorough due diligence process is designed to prevent.

Your Top Questions Answered: Buying a Home in Portugal

Buying property in another country always comes with a lot of questions. Let's tackle some of the most common ones that pop up for international buyers looking at Portugal.

Can Foreigners Even Buy Property in Portugal?

Yes, and it's surprisingly straightforward. Portugal welcomes foreign buyers with open arms, and there are no special restrictions whether you're from the EU or not.

The one absolute must-have for any foreign buyer is a Portuguese tax number, known as a NIF (Número de Identificação Fiscal). You'll need this before you can sign any contracts, so it's one of the very first things you'll sort out.

What Are the Ongoing Costs I Should Expect?

Once you have the keys, the costs don't stop. It's crucial to budget for these recurring expenses.

Your main annual expense will be the IMI (Imposto Municipal sobre Imóveis), which is the municipal property tax. It's a small percentage of your home's registered tax value.

If you own an apartment or a house in a planned community, you'll also have condominium fees. These cover the maintenance of common areas like gardens, pools, and elevators. On top of that, you have the usual suspects: utility bills and homeowner's insurance.

Realistically, How Long Does the Whole Process Take?

From getting your offer accepted to finally holding the keys, you should plan for about two to three months.

This timeframe gives your lawyer enough breathing room to conduct all the necessary due diligence, for you to sign the promissory contract (CPCV), and to get your financing squared away if you're taking out a mortgage.

A word of warning from experience: delays often happen because of missing paperwork on the seller's end, like an out-of-date habitation license. A good lawyer will spot this early, which is exactly why you should never rush the legal checks.

Should I Get a Mortgage in Portugal or Back Home?

This is a great question, and there's no single right answer. It really depends on your circumstances.

- A Portuguese mortgage can be simpler because local banks understand the property laws and processes inside and out.

- A mortgage from your home country might offer more competitive interest rates or terms you're more familiar with.

The best approach? Explore both options. Talk to a mortgage broker in Portugal and also have a conversation with your bank back home. Compare the offers and see what makes the most financial sense for you.

Ready to turn your dream into a reality? Start exploring properties across the country with Residaro. From sun-drenched villas in the Algarve to chic apartments in Lisbon, your perfect Portuguese home is waiting. Begin your search on Residaro.com.